Is Shorting Apple A Good Idea?

It Seems Heretical And A Sure Way To Lose One's Shirt

Unless you are a market maker who acts with a privileged view of existing bid and ask prices, decisions about investing or trading require an opinion about the future of an asset’s price. Such decisions are subject to uncertainty, so they are basically bets. A lot of mathematics can be applied to reduce the uncertainty, but in the end every bet will be some variation of buy low, sell high.

It is hard to resist the feeling of financial assets being overvalued after a long stretch of price increases. As of today, the NASDAQ 100 has risen by 47% in the last 12 months, and Apple’s stock price has gone up by 33% in the same time span. The old adage of what goes up must come down rings in the back of the brain. But then, such wisdom often leads to missed opportunities and bigger calamities. Carl Icahn, who could do no wrong for a long time, admitted to losing $9B with a long-time short bet on the markets (a 47% notional short on his sizable portfolio in 2022).

Back in 2012, we got infected by abundant pessimism, becoming convinced that the markets had become too exuberant after the Great Financial Crisis. After running up some sizable losses, we found solace in expert opinions, such as the Hussman Funds’ market comments. According to those, the market was a perfectly doomed sextic polynomial function. We increased our short until we ran out of money to lose.

In the last year, we engaged in some opportunistic trading in /NQ (Nasdaq 100) futures, mostly on the short side. End of October 2023 was a great opportunity for a long trade, but it felt too awkward to switch our minds to optimism - big mistake. With inflation and interest rates coming down (or at least not going up) and the economy going strong, we have no good reasons to assume that /NQ is bound for a major fall in 2024, aside from the occasional 2-5% blip. But, as the great German writer and caricaturist Wilhelm Busch once wrote: “Erstens kommt es anders, zweitens als man denkt” (It never happens as you expect).

There are multiple problems with shorting an index except for short term trades: A) long term and outside China, the market mostly goes up and B) even the Nasdaq 100 which is 50% dominated by 7 stocks offers decent diversification and the markets’ breadth is not as narrow as it seems. So we looked at Apple, in our desire to bet against something.

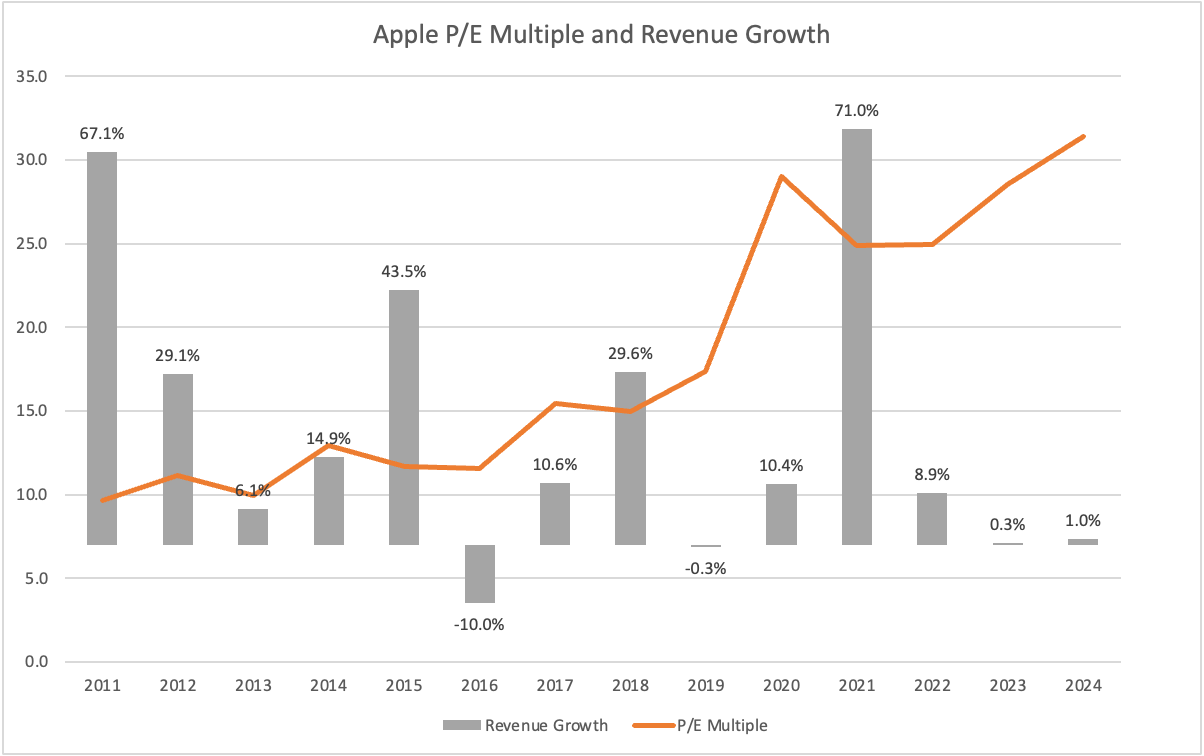

A long term Apple investor has enjoyed cumulative annual returns of close to 25% since Steve Job’s death in October of 2011, despite ominous predictions of stagnation in the absence of the master (“Sell the stock, the man is dead”, Barron’s). Apple’s price/earnings multiple (P/E) has expanded from the low 10s to the 30s in the last dozen or so years, despite sometimes choppy revenue growth (12% average growth):

The theory behind Apple’s expanding multiple is its service business and the presumed economies of scale that should come with it. Apple’s service business (App Store, Apple Pay, Apple Card, Apple TV+, Apple Music, Apple Arcade, iCloud, advertising; and payments from Google for search) accounts for about 25% of Apple’s total revenue of $383B, as of Q3 2023. When it comes to Apple’s products and their growth prospects, there is a rich cottage industry of analysis and we don’t plan to contribute to that. Suffice to say that the company is not doomed, the expensive VisionPro could be a nugatory failure and people keep buying the Apple watch (which was predicted to be a dud as well) despite some missing functionalities.

If a company’s growth rate is suspiciously lower than it’s P/E multiple, another old adage comes to mind. Peter Lynch, whom I still remember from reading Barron’s weekly 200 pages, which always left ink on my fingers, popularized the concept: "The P/E ratio of any company that's fairly priced will equal its growth rate" (One Up on Wall Street, (2000)). Now, that’s a little simplistic and no company can grow 30% in perpetuity without exceeding the size of the universe (because it’s exponential growth).

In the last dozen years, Apple grew 12% on average and maintained a constant net earnings margin of 20 to 25%, thanks to an impressive range of overpriced and addictive products. The last three years don’t point to a continuation of that average, but investors seem to keep up the hope for now.

If Apple gets back to near term growth of 10% per year, it could be valued around $2.6T - relatively close to it’s current valuation of $3T (with some assumptions, i.e., growth tapering off to 5% after 10 years, discount rate of 10.5%, constant margins of 25% etc.). If growth turns into a constant 5%, which looks more likely, Apple’s value should be in the order of $1.7T - much lower.

Valuations are an imperfect predictor of price changes and unsuitable for trading. On Feb 2nd, after the close, Apple will publish its Q4 earnings. Apple is predicting almost no growth for 2024, and we believe that markets are efficient. All information should be baked into the current stock price, although we have seen several incidents recently where this was clearly not the case.

The thing with valuations is that they are based on expectations - of growth, margins, risk and other factors. Most shareholders don’t have explicit expectations for Apple’s growth that make them think that Apple’s stock price is right. A few smart ones probably do, while the rest looks left and right for assurance and comfort. And sometimes things change and the market corrects its implicit expectations in a very short time frame. We cannot fight the thought that Apple is an overextended rubber band that may snap in the hands of its investors soon.

Disclaimer: Views that we are expressing in this article are our own. We are not a licensed securities dealer, broker or US investment adviser or investment bank. Neither are we licensed or certified by any institute or regulatory body. This article does not constitute a recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person.